Market Overview

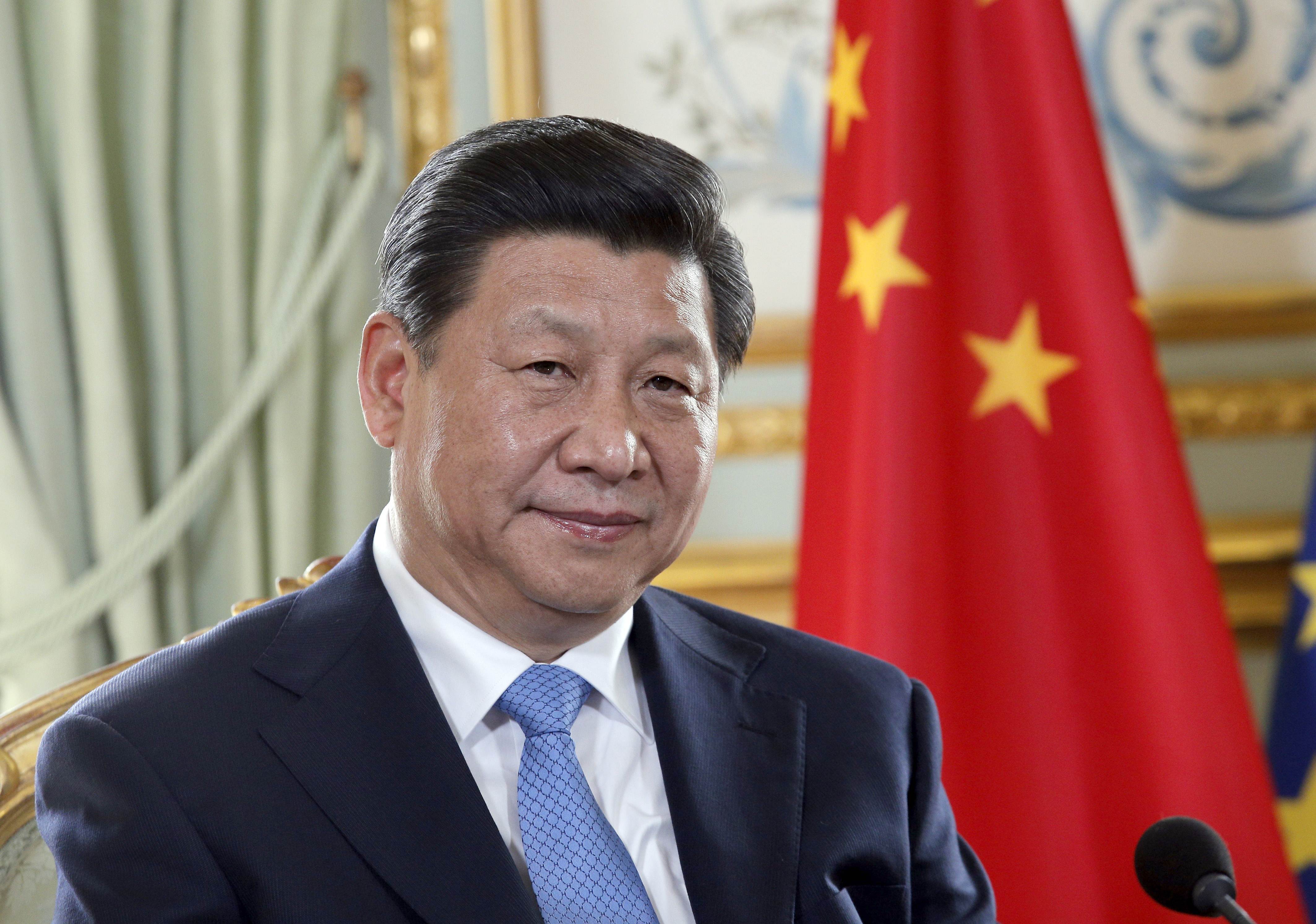

Prediction markets are assigning a 2.2% probability to the removal of Xi Jinping as China's General Secretary before the end of June 2026, with roughly $2 million in trading volume supporting relatively stable odds. This minimal probability has held steady over the past day, indicating consistent market sentiment around what traders view as an extremely unlikely scenario within an 18-month window. The market's definition of removal is broad—encompassing resignation, dismissal, detention, disqualification, or any circumstance preventing Xi from fulfilling his duties—yet even this inclusive framing has not materially elevated the odds.

Why It Matters

Xi's position as General Secretary represents the apex of power in China's political system, and the continuity or disruption of his rule carries significant implications for global geopolitics, economic policy, and regional stability. Any unexpected change in Chinese leadership would likely trigger market volatility across asset classes, given the potential for shifts in foreign policy, trade relations, and domestic economic priorities. The low odds assigned to this scenario reflect broad market confidence in Xi's political security, though the question implicitly acknowledges that even entrenched leaders face non-zero risks from health crises, internal party conflicts, or unforeseen institutional challenges.

Key Factors

Several structural factors support the market's assessment of minimal removal risk. Xi has consolidated significant control over the Communist Party, the military, and state institutions since assuming power in 2012, eliminating many traditional mechanisms through which Chinese leaders faced sudden ouster. The party's succession planning processes, while opaque to outsiders, appear to operate on multi-year timelines rather than emergency protocols. Xi's age—he is 71—and general public health status show no widely reported signs of imminent incapacity. Additionally, the 20th National Congress in October 2022 resulted in Xi's unprecedented third term as General Secretary, signaling party consensus around his continued leadership through at least 2027.

However, the 2.2% probability does price in tail risks that markets acknowledge as non-negligible. These include sudden serious illness, unexpected internal party factionalism escalating to critical levels, military or security apparatus unrest, or economic crises severe enough to trigger institutional intervention. China's political system, despite appearances of stability, remains opaque to external observers, and historical precedent shows that even seemingly entrenched leaders can face rapid reversal—though such transitions are exceptionally rare in modern China.

Outlook

For the probability to materially shift upward, markets would likely require either credible reporting of Xi's serious health decline, visible signs of major party factionalism, significant instability in state security institutions, or an economic crisis of unprecedented scale. The current pricing reflects a baseline assumption of continuity in Xi's leadership through mid-2026, with only marginal allowance for unexpected disruption. Traders monitoring this market would primarily track Chinese state media for any signals of institutional stress, international reporting on Xi's health and public appearances, and broader indicators of party cohesion or factional tension—though such information flows from China remain limited and difficult to interpret with precision.